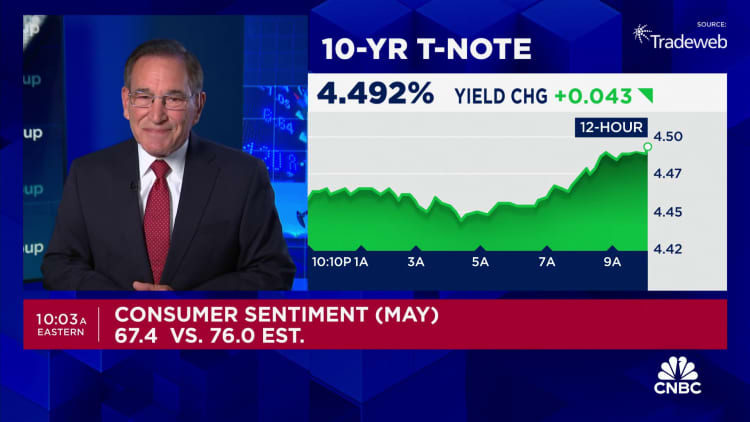

Consumer sentiment slumped as inflation expectations rose, despite otherwise strong signals in the economy, according to a closely watched survey released Friday.

The University of Michigan Survey of Consumers sentiment index for May posted an initial reading of 67.4 for May, down from 77.2 in April and well off the Dow Jones consensus call for 76. The move represented a one-month decline of 12.7% but a year-over-year gain of 14.2%.

Along with the downbeat sentiment measure, the outlook for inflation across the one- and five-year horizons increased.

The one-year outlook jumped top 3.5%, up 0.3 percentage point from a month ago to the highest level since November 2023.

Also, the five-year outlook rose to 3.1%, an increase of just 0.1 percentage point but reversing a trend of lower readings in the past few months, also to the highest in November.

“While consumers had been reserving judgment for the past few months, they now perceive negative developments on a number of dimensions,” said Joanne Hsu, the survey’s director. “They expressed worries that inflation, unemployment and interest rates may all be moving in an unfavorable direction in the year ahead.”

Other indexes in the survey also posted substantial declines: The current conditions index fell to 68.8, down more than 10 points, while the expectations measure fell to 66.5, down 9.5 points. Both pointed to monthly drops of more than 12%, though they were higher from a year ago.

The report comes despite the stock market riding a strong rally and gasoline prices nudging lower, though still at elevated levels. Most labor market signals remain strong, though jobless claims last week hit their highest level since late August 2023.

“All things considered, however, the magnitude of the slump in confidence is pretty big and it isn’t satisfactorily explained by” geopolitical factors or the mid-April stock market sell-off, wrote Paul Ashworth, chief North America economist at Capital Economics. “That leaves us wondering if we’re missing something more worrying going on with the consumer.”

The inflation readings represent the biggest pitfall for policymakers as the Federal Reserve contemplates the near-term path of monetary policy.

“Uncertainty about the inflation path could suppress consumer spending in the coming months. The Fed is walking a tightrope as they balance both mandates of price stability and growth,” said Jeffrey Roach, chief economist at LPL Financial. “Although it’s not our base case, we do see rising risks of stagflation, a concern the markets will have to deal with, in addition to the impacts from the presidential election.”

At their meeting last week, Fed officials indicated they need “greater confidence” that inflation is moving “sustainably” back to their 2% goal before lowering interest rates. Policymakers consider expectations a key to taming inflation, and the outlook now from the Michigan survey has sown consecutive months of increases after falling considerably between November and March of this year.

Market pricing is pointing to a strong expectation that the Fed will begin reducing its key borrowing rate in September after holding it at its highest level in more than 20 years since July 2023. However, the outlook has been in flux even with Fed Chair Jerome Powell indicating in his post-meeting news conference that it is unlikely the central bank’s next move would be hike.

The next important data point for inflation comes Wednesday when the Labor Department releases its consumer price index report for April. Most Wall Street economists expect the report to show a slight moderation in price pressures, though the widely followed CPI index has been running well ahead of the Fed’s target, at 3.5% annually in March.